What Is Commercial Bridging Finance in Property Investment”

Commercial property deals in the UK move quickly. Sometimes uncomfortably quickly.

A developer spots an undervalued office block. An investor wins a mixed use property at auction. A landlord finds a retail unit in a prime location, but the bank says funding could take two months. By then, the opportunity may already belong to someone else.

That pressure is exactly why commercial bridging finance has become such an important tool in modern property investment.

For experienced developers and first time investors alike, it offers short term funding that can often be arranged far faster than traditional mortgages. Used correctly, it helps buyers secure profitable opportunities, refurbish properties, or avoid expensive delays.

So, what is commercial bridging finance, and how does it actually work in real property transactions?

What Is Commercial Bridging Finance?

Commercial bridging finance is a short term secured loan designed to help borrowers purchase or refinance commercial property quickly.

The loan is usually secured against:

- Offices

- Warehouses

- Shops

- Industrial units

- Hotels and guesthouses

- Semi commercial properties

- Land with commercial value

Unlike standard commercial mortgages that may take several months to process, bridging finance commercial property loans are designed for speed and flexibility.

Most loans run between 3 and 24 months.

The borrower repays the loan through a planned exit strategy, which usually involves:

- Selling the property

- Refinancing onto a long term mortgage

- Releasing equity from another asset

- Using business or investment income

Bridging finance is not intended as permanent borrowing. It is temporary funding designed for situations where timing matters.

Also Read – Using Secured Bridging Loans for UK Property Purchase and Renovation

Why Investors Use Commercial Bridging Finance

Property investors often operate in unpredictable conditions. Delays happen. Chains collapse. Auction deadlines arrive quickly.

Traditional lenders are usually cautious with unusual properties or urgent transactions. Bridging lenders tend to take a more practical approach by focusing heavily on the property value and the borrower’s exit strategy.

That flexibility makes commercial bridging finance useful in several situations.

Buying Auction Properties

Auction purchases in the UK commonly require completion within 28 days.

A high street bank may struggle to complete underwriting, valuations, and legal checks within that timeframe. Bridging lenders are structured for faster transactions.

Funding Refurbishment Projects

Many commercial buildings are unsuitable for traditional mortgages because they require major repairs or renovation.

For example:

- Vacant office buildings

- Uninhabitable mixed use properties

- Empty pubs or retail units

- Properties without functioning kitchens or bathrooms

Bridging finance allows investors to purchase and improve the property before refinancing later.

Preventing Broken Property Chains

Commercial transactions sometimes collapse because another sale is delayed unexpectedly.

A bridging loan can provide temporary liquidity while the borrower waits for another property sale to complete.

Property Conversion Projects

Developers frequently use bridging finance for projects involving:

- Office to residential conversions

- Shop to flat conversions

- Mixed use redevelopment

- Semi commercial refurbishments

After completion, many borrowers refinance through a commercial mortgage agent to secure long term funding.

Bridging Finance Examples for Property Buyers and Investors

Example 1: Commercial Auction Purchase

An investor purchases a vacant retail property at auction for £420,000.

The lender requires a 30 percent deposit, while the remaining balance is funded through commercial bridging finance. The deal completes within two weeks, allowing the buyer to meet the auction deadline.

After refurbishing the property and securing tenants, the investor refinances onto a commercial mortgage.

Example 2: Semi Commercial Conversion

A developer buys a property containing a ground floor shop with unused upper floors.

Because the upper floors require structural work, mainstream lenders decline the application. A bridging lender approves short term funding based on the property’s future value and refurbishment plan.

Once the flats are completed and rented, the borrower exits the bridging loan using long term finance.

Example 3: Chain Break Protection

A landlord plans to buy a warehouse conversion project, but the sale of another commercial property is delayed because of legal issues.

Rather than losing the purchase opportunity, the borrower uses temporary funding through bridge loans UK investors regularly rely on for time sensitive transactions.

What Do You Need to Apply for Bridging Finance?

Commercial bridging finance applications are usually more flexible than traditional mortgage applications, but lenders still carry out detailed risk assessments.

Most lenders will request:

- Proof of identity and address

- Details of the property

- Property valuation

- Bank statements

- Evidence of income or assets

- Credit history information

- A clear exit strategy

The exit strategy is one of the most important parts of the application.

Lenders want evidence showing exactly how the loan will be repaid at the end of the term.

For development or refurbishment projects, lenders may also review:

- Planning permission

- Contractor quotations

- Development timelines

- Projected end values

Many investors also use a bridging loan calculator UK before applying to estimate borrowing costs and monthly interest.

Which Lenders Offer Fast Commercial Bridging Finance?

The UK bridging market includes specialist lenders, challenger banks, and private funding providers.

Different commercial bridging finance lenders specialise in different areas, including:

- Heavy refurbishment

- Auction purchases

- Land finance

- Semi commercial properties

- Adverse credit cases

- Large portfolio lending

Some lenders focus heavily on speed, while others prioritise lower interest rates or higher loan to value ratios.

Working with an experienced broker often improves lender selection because they understand which lenders suit specific property types and timescales.

Investors planning a refinance later may also compare commercial property mortgage rates early to build a realistic exit strategy.

Also Read – How Do Property Development Loans Work in Real Estate Projects?

Are Residential Bridging Loans FCA Regulated?

Yes, some bridging loans in the UK are regulated by the Financial Conduct Authority (FCA).

Regulation depends mainly on how the property will be used.

A bridging loan is usually FCA regulated when:

- The borrower lives in the property

- The borrower plans to live in the property

- An immediate family member occupies the property

Purely commercial or investment focused bridging loans are generally not FCA regulated.

For example:

- A loan secured against a buy to let commercial investment is usually unregulated

- A loan secured against the borrower’s own home is usually regulated

Understanding this distinction matters because regulated loans involve additional consumer protections and stricter compliance standards.

Developers moving into residential schemes may also consider a residential property development loan for larger construction projects.

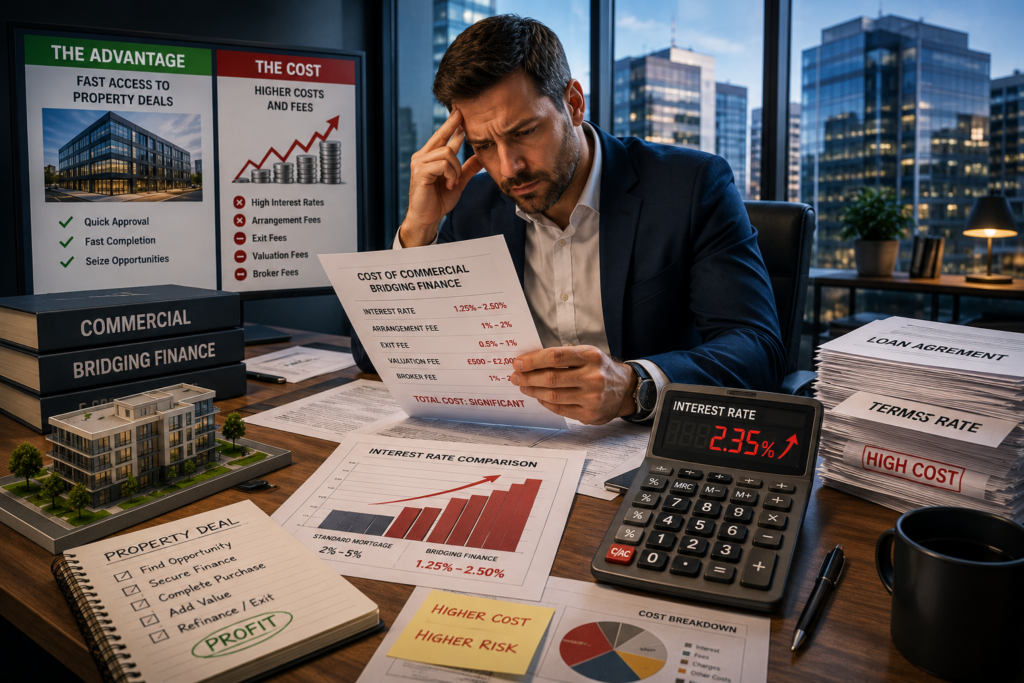

Is Commercial Bridging Finance Expensive?

Compared with standard commercial mortgages, bridging finance is generally more expensive.

Interest rates are higher because lenders are offering:

- Faster approvals

- Greater flexibility

- Short term risk exposure

- Funding for unusual or unmortgageable properties

Typical costs may include:

- Monthly interest

- Arrangement fees

- Valuation fees

- Legal fees

- Broker fees

- Exit fees in some cases

However, experienced investors usually assess bridging finance based on opportunity value rather than headline rates alone.

Losing a profitable commercial property deal because finance arrived too slowly can easily cost more than the bridging loan itself.

Conclusion

Commercial bridging finance gives UK property investors access to fast, flexible funding when traditional lenders cannot move quickly enough.

It is widely used for auction purchases, refurbishments, chain breaks, and commercial conversions because it allows borrowers to act decisively in competitive markets.

Successful investors approach bridging finance carefully. They calculate costs properly, choose lenders strategically, and build realistic exit plans before borrowing.

When used intelligently, commercial bridging finance becomes more than short term lending. It becomes a practical investment tool that helps property buyers secure opportunities that slower finance simply cannot support.

FAQs

- What is commercial bridging finance mainly used for?

Ans. Commercial bridging finance is mainly used for buying, refurbishing, or refinancing commercial property quickly before arranging long term funding or selling the asset.

- How long do commercial bridging loans last?

Ans. Most commercial bridging loans last between 3 and 24 months, depending on the lender and the borrower’s exit strategy.

- Can you get bridging finance for unmortgageable properties?

Ans. Yes. Bridging lenders often fund properties that traditional lenders reject because of poor condition, structural issues, or incomplete refurbishment.

- Are commercial bridging loans regulated by the FCA?

Ans. Purely commercial bridging loans are generally not FCA regulated. Loans secured against properties occupied by the borrower or family members are usually regulated.

- Do bridging lenders check credit history?

Ans. Yes. Most lenders review credit history, but many are flexible if the property deal and exit strategy are strong.

Discover the Latest Trends

Stay informed with our latest articles and resources.